If you ever looked down on those uncles staring at the fine print, pulling down the spectacles down the ridge of their nose, and asking at the counter,

Ah auntie, how much cashback ah?

That’s me.

If you thought the people who go reading online reviews on cashback, and finance, on the weekend, for fun, were crazy, yes I’m probably that crazy.

It’s all in the name of retiring before 40.

Just don’t date me. I would probably wax lyrical about the latest cashback you can get from your card.

And I would probably tell you that we should probably go to the hawker centre, rather than the mall.

Having held as many as 7 different debit cards (don’t laugh), I’m here to tell you what has been the best experience for me, and how you can maximise your cashback.

| The debit cards I’ve held | Great | Not great |

|---|---|---|

| DBS Visa (or Multicurrency) Debit Card |

No fall below fee There’s a multi-currency wallet, although you do need to waste time exchanging currencies virtually. |

3% cashback on local transport (Ride-hailing, taxis, Transit – Simply Go) Valid with a minimum of S$500 on Visa and cash withdrawals limit of S$400 and below in the same month. Banking app loads slowly at 4.67s just to reach the signed in page. |

| DBS PAssion Debit Card | 4% rebate at Cold Storage, Giant and Guardian, but now with 8% cashback when linked to Yuu rewards club | Minimum of $400 spending needed, and cash withdrawals of less than $400 in a single month |

| GXS Bank |

No fall below fee Bank app is the fastest to load amongst all the local banks |

Functionality is limited on the app (you can’t do scheduled or regular payments, for example) |

| Trust Debit Card |

No fall below fee The foreign exchange fees is hands-down, one of the best, and even better than market leaders Wise, because of how convenient it is. Whilst Wise does offer a percentage point difference in terms of savings, it doesn’t make sense in terms of the time you save by checking out immediately with Trust. |

Cashback is in the form of rebates |

| OCBC Frank Debit Card | 1% cashback |

Minimum of $1000 needed, or not fall below fees of $2 are charged Bank app takes about 4.7s to sign in. |

| UOB One Debit Card (I use this) |

High cash back of 3%, with minimum $500 The bank app loads the fastest, at 2.95 seconds, compared to the usual average of 4.5s amongst the other traditional banks. Short (or often no) queues at the ATM, and you can even use the OCBC ATMs at no extra charges too! |

Average monthly balance of $500 needed in the bank account, or fall below fees of $2 charged |

| Wise Debit Card | Ideal if you’re spend regularly on overseas transactions, as they have one of the cheapest fees | But you have to top up your card and go through the hassle of transferring money into your Wise account |

Think of debit cards as extensions for your hands

Here’s an easy way to think of debit cards. They are like extensions for your hands to grab things you want. But there’s a caveat. Every time you grab something, money flows out of you.

So the debit card also becomes like a little channel of money flowing out of you. If you have this river of money flowing out of you, you would also want a sieve that returns some of the money to you.

You need them to do the following:

And frankly, that’s it.

If we’re honest, most of us probably use credit cards to pay contactless. The only places where we would still use debit cards are those that don’t accept PayWave (because the Visa/Mastercard charge can be a hefty 6% for merchants).

That also means that often, the most important thing to think about isn’t cashback.

It’s convenience.

Think about convenience, not cashback

That’s why if you have no time to read the rest of the article, I will simply show you this graph of app loading times.

UOB is the fastest.

And for those times that you want to do PayNow, they even directly push you there to key in the person’s details, without you needing to first authenticate. This is much faster than DBS or OCBC.

What’s more, the time you need cash is reduced by the shorter queues at UOB ATMs, which is supplemented by the OCBC network of ATMs. Both OCBC and UOB ATMs can be withdrawn from, using a UOB debit card.

Of course, you might still want to use the credit card… but here’s some well-meaning advice.

Debit cards are still better than credit cards

Credit, really isn’t that sexy.

For all the free gifts they might throw at you, read the fine print. You may need to:

- spend $500 in the first month

- hold onto the card for a year

All these are the ways that banks use to make sure they make money off you, before you leave.

They are there to hook you. After all, spending money makes you feel powerful. Bring home the latest MacBook, the newest iPhone, and you start feeling like you’re the sexiest guy in the room.

But it’s not the best way to sustain a financially wise life.

I’m still wary whenever I use a credit card. Not without good reason.

Ultimately, there are certain red lines in my financial management. I refuse to spend money I don’t have. Or spending money that I have, that I can pay later.

It’s just too far a slippery slope for me. And knowing how dangerous that can be, I would rather not put a ticking grenade in my pocket.

That’s why I stick to debit cards. They can help you to spend more reasonably, rather than trying desperately to get the next cashback, over and over again.

There are many ifs.

To maximise your cashback, you need to ask yourself some questions:

- Which grocery store do you most regularly shop? The most common cashback cards offer cashback mostly at NTUC Fairprice, with the Trust Debit Card or the Dairy Farm group of stores (Cold Storage or Giant), with the UOB Debit Card.

- How do you usually pay for travel? Is it via EZ-Link topup, or debit card?

Here are some principles if you want to get the most cashback.

Keep most spending to a single card

Grocery, travel, and online shopping can all be kept to a single card. Rather than switching between your various cards, I would recommend that you keep the spending in a single card so that you can maximise cashback.

After all, when all you’re getting back is a few dollars a month (3% of $400 spent is about $12), you might not find it worth to split your hairs on spending on other things.

Don’t pressure yourself to reach the limit

If you’re honest, it’s not that easy to hit card transactions of $400 a month.

My card transactions have been about $300 a month. $150 for food, and $150 for personal expenses.

Look at it this way. If you were able to spend just $40 a week in secondary school, what makes life in the workplace different?

Not much.

Just because you earn more money, doesn’t mean you need to spend it.

Hands-down, the UOB One card

Since the last time I wrote, the UOB ONE Debit card has tightened its spending criteria, meaning that you do have to hit $500 now.

I’ve used this since I was a pimply 16-year-old.

As a 16-year-old, I would be that nerd who would go down to the bank with his passbook, put in the hard-earned cash after a day of backbreaking work arranging bottles at a supermarket, and then see the money slowly inked into the passbook.

It was cute, but it also made me fall in love with UOB.

Over the years, it’s been the card of choice for everything. Transport, grocery, and even my regular internet purchases.

It’s the card of choice for me, because of how consistent it has been with the cashback. At the start of each month, on the 1st, the cashback is immediately credited into your account.

What I also love is that the fall below fee is only if your balance drops below $500, which is lower compared to the other cards like OCBC.

Imagine staring at the stupid DBS icon, with its rotating hexagons, every other day. You might want to PayNow a friend for a meal you had with them.

Or check if your pay is in. If you add the seconds, it’s a lot of hours spent waiting for your bank to load.

Forget DBS. Over and over again, UOB is the fastest.

The Trust Card is a close second for its base 1.5% savings interest rate

Trust, the newest digital bank on the block, is actually, great.

For all the complaints about waiting time, I got mine in 2 weeks.

What’s more they actually tell you where the card is.

Beyond the NTUC LinkPoints you get when you check out, the best thing is the user interface.

This is a mobile-first bank, meaning, there’s no banking website (yet).

But it also means that the app’s interface is beautifully thought through, with small details like the welcome page greeting you with a ‘huat ah!’ during Chinese New Year being a nice afterthought.

Some users have complained that the Trust Bank’s user interface is not that user-friendly, with basic functions such as how to find where to register your PayNow number on the app being not so easy.

I concede.

It’s not.

What can also be irritating will be the email, after email, after email, you get from them for every transaction you make.

Yup.

Took a bus?

They will email you ‘Yay! Your transaction went through.’

Initially, it was fun, but later… it’s not.

But Trust Bank’s greatest benefit – is its 1.5% interest rate.

No special deposit needed. No minimum sum.

It’s also beautiful to see how their interface automatically classifies the different spending categories. For me, that’s been helpful in terms of budgeting, and seeing where my money is being spent.

Automatic categorisation of spending is quite cool

For example, as you can see from the above, the Trust app sorted my spending into its respective categories. This helps when you’re trying to see where you’re close to bursting your budget.

From what I’ve seen from the other banking apps, Trust is the only one that can automatically sort.

How about GXS or Maribank?

I’ve used both GXS and Maribank.

Maribank does not have a debit card option, with their only card being a credit card.

You should use them if you’re searching for good savings rates. GXS has 2.68% in their savings pocket whilst Maribank has 2.7%.

I used the GXS Debit Card for a whilst because they had bonus cashback, but after a while, I stopped. It didn’t make sense because there were not many special partnerships they had with merchants. So beyond being a channel for money to flow out of money, there was no other reason.

The home (not my) favourite is the DBS PAssion card, which offers points-back, but little cashback

Everyone knows the DBS PAssion card, but that doesn’t mean you have to stick with it.

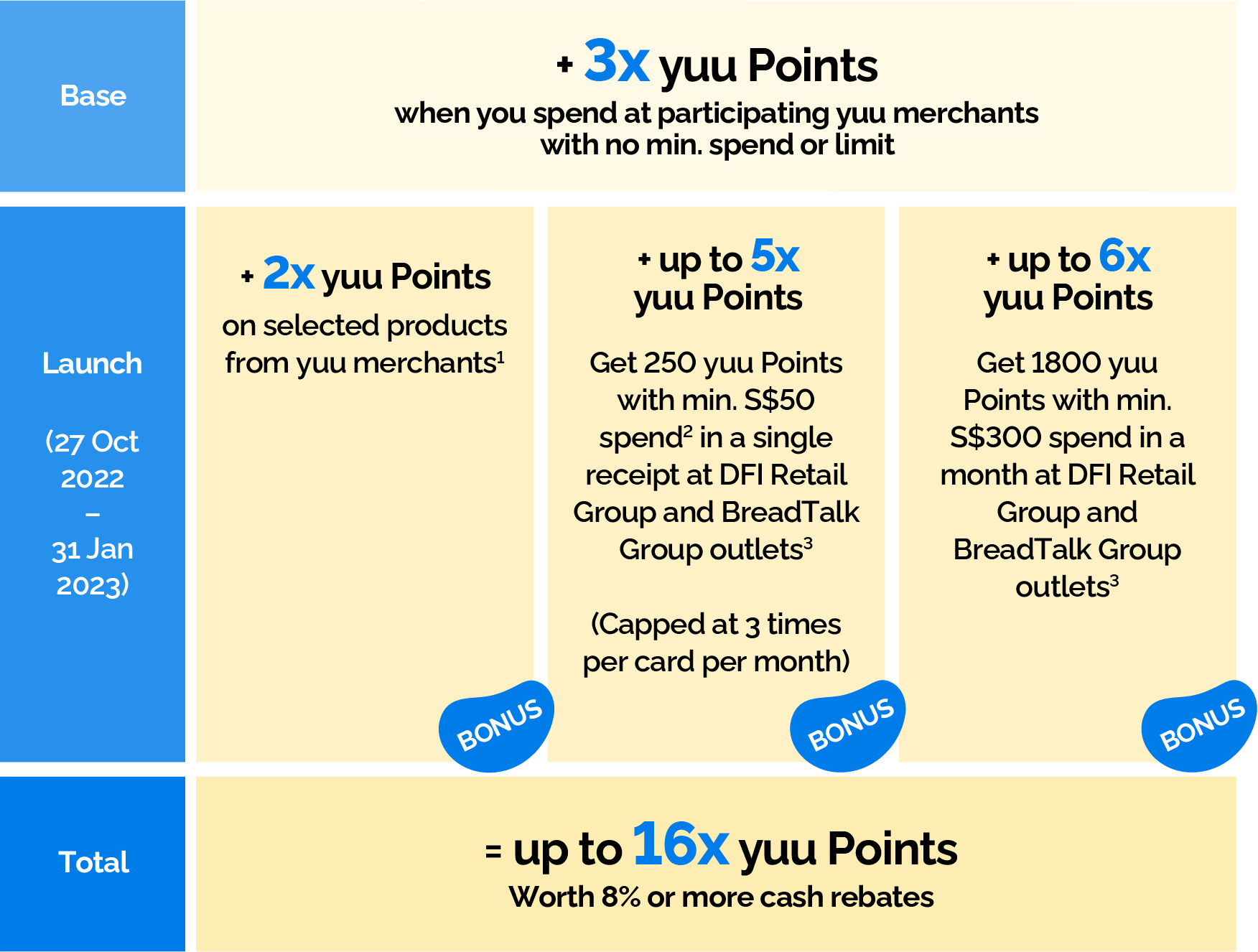

DBS has recently upped its game with the recent October 2022 launch of the Yuu card. But to qualify, you need to spend a minimum of $400 a month.

For me, DBS is just the bank that gave fancy treats this year like the $3 complimentary Friday Hawker meals via PayLah. But beyond that their marketing, the experience is pretty hard.

Go to their bank branch, and you have to queue.

Take money, and you have to queue.

Gosh, it’s much better to just get a UOB or OCBC card.

Use OCBC Frank, if you want fancy card designs

There’s no great cashback for the OCBC Frank. Only a fancy card design you can show off.

Well, if you don’t have the money, at least you can show off the card, heh?

I’m kidding. The OCBC Frank Card is not a card I would personally recommend, because of the low cashback, and the $1000 you have to keep inside (or risk fall below fees of $1000).

Whilst OCBC did have a previous attractive offer of the NTUC Debit Card, with a cashback of almost 8%, that’s ending. In Feb 2023, no more 8%!

Maybe OCBC realised they weren’t cashing back more money than they were making!

Get the UOB One Card

Most of us don’t really want to spend our lives reading through terms and conditions, trying to figure out just how much cashback you will get.

I mean, if you were spending thousands of dollars each month, sure, the difference between 3 and 4% will make a difference.

But for the rest of the commoners like you and me, it will probably not make that much difference. What matters more is taking an effort to

- Grow your income

- Know every single penny that goes out

- Control your expenses on non-discretionary, luxury, products

- Build wealth

That will help you grow your income over time.

Look no further. UOB One is really the only one you need.

According to UOB, it states: “Enjoy 3% cashback on Dairy Farm International (“DFI”) transactions (Cold Storage, CS Fresh, Giant, Guardian, 7-Eleven, Marketplace, Jasons and Jasons Deli), 3% cashback on Shopee Singapore transactions (excludes ShopeePay), 3% on SimplyGo (bus and train rides) & 1% cashback on Grab transactions (excludes mobile wallet top-ups) with a minimum monthly spend of S$500. Cashback is capped at S$20 per calendar month across DFI, Shopee Singapore, SimplyGo & Grab transactions. Click here for UOB One Debit Card Terms and Conditions.”

when I checked on the uob website, it states cashback will only be awarded with a monthly spend of 500$, tested the theory by using the cashback calculator on their website and it doesn’t award cashback when spend is below 500$, did they change their policy?

Hi John! I use the UOB One Debit Card as my main card and have gotten the cashback monthly, even when my spend is under $500. You can try it yourself and see what happens. Hope this helps 🙂

I’m confused based on your chart and UOB 1 debit card it says that you are required to spend a minimum of $500 in order to qualify for the cashback

But you said and I quote

“What’s even better is that the 3% cashback has no minimum spend. You don’t feel the pressure to spend more than $400 a month just to qualify for cashback.”

So do u need to hit the minimum spending or not ? 😂

Hey thanks for pointing that out! I should have clarified – you need a balance of $500 in the bank account, or you will be charged fall below fees. But there’s no minimum spend required. Hope this helps!