It suddenly seems like many REITs are raising money from the stock market.

On 1 June, IREIT announced their rights issue to finance the acquisition of retail parks. Then CapitaLand India Trust (CLINT) announced 119 for every 1000 units, at a price of $1.06.

This means that if you have 3000 units, you can buy 357 (3 x 119) units for $378.42.

And you might be thinking if it’s really worth holding onto more of CLINT, especially in a time when their share price has heavily fallen over the year. At this point there are 3 things you can make.

- Choose not to subscribe to their rights issue

- Subscribe to their rights issue

- Sell off CLINT

Here’s how to think about it, and when rights issues do make sense.

It’s not just about the yield accretion

REITs are extremely good at selling ‘yield-accretive’ opportunities. They often give you neat and tidy graphs about how their yield will improve.

But they don’t tell you about what happens to their share price.

It often drops. And that’s only to be expected, especially with an enlarged base of units.

Whilst your earnings might increase, there’s also a much bigger base of units to spread those earnings with.

Simple math.

An analogy to compare the rights issue

Let’s say you want to buy a house to rent out. The house costs $1 million in total.

You can’t afford it on your own.

You go to a friend to ask him to share in the costs of paying for the home.

He agrees.

You have to share the rental with 2, instead of one now.

That would split your rental collections in half, rather than the proposed 100% to you.

Not just yield accretive, but capital appreciation too

Ultimately, what determines returns for a stock?

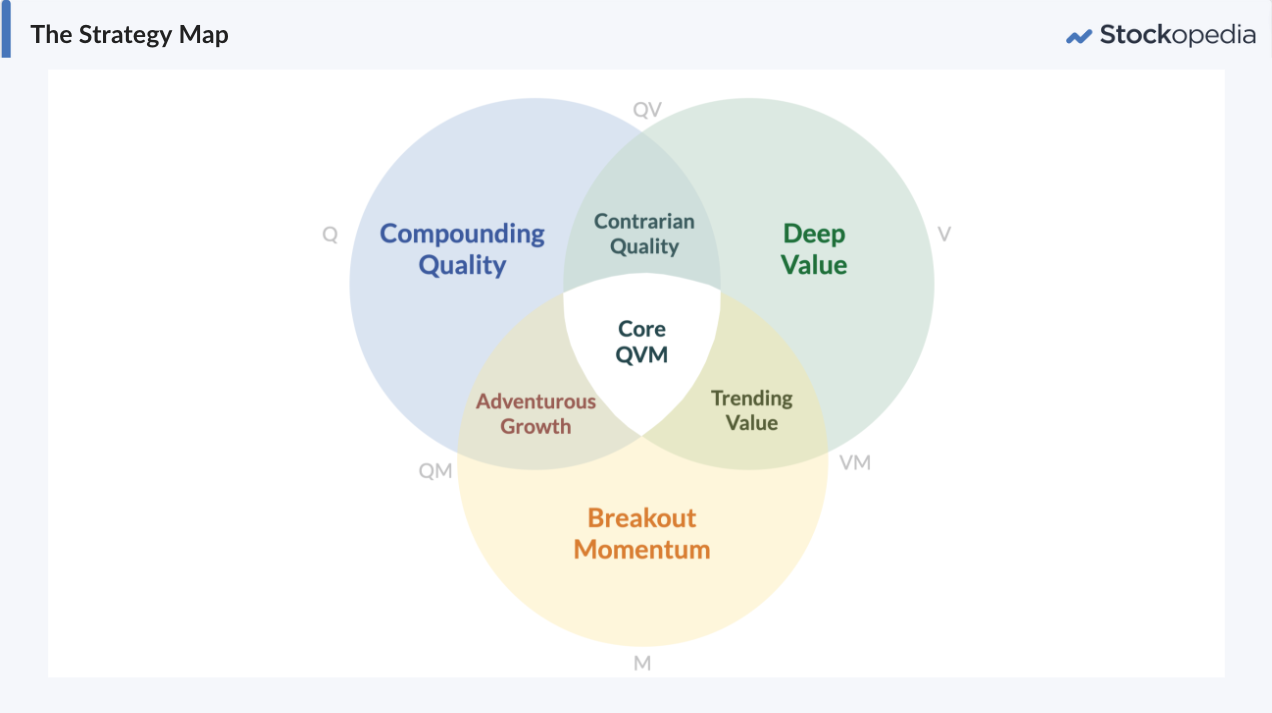

According to Ed Croft, the founder of Stockopedia, a stock screening software, there tends to be three factors that eventually drive share prices up.

Value, momentum, and quality.

Value means cheap.

Momentum means the share price is growing.

Quality means the stock’s business is good.

How does this work for REITs though?

I will be the first to confess that for the 4 REITs that I’ve owned in First REIT, IREIT Global, Frasers Commercial and Logistics Trust, and CLINT, only FLCT has yielded me positive returns in both capital and yield appreciation.

The potential momentum in share price from the rights issue

If we simply look at the rights issue, and how it represents 10.6% of the current units in issue (meaning the number of shares being traded on the market), the current rights issue could potentially stymie the growth of the stock price.

Especially when it’s offered at a discount.

The Issue Price of S$1.060 represents a discount (the “Issue Price Discount”) of 6.0% to the volume-weighted average price1 (“VWAP”) of S$1.1279 per Unit.

We do know that CLINT’s share price has fallen drastically in recent weeks. Relative to its peers though, it has fallen less.

One might argue that they weren’t as high compared to the other stocks we are comparing them too.

But it bears noting that the market still sees value in their business model of providing quality properties to companies in India, and it thus hasn’t beaten down their share price yet.

Whether you see that in them, is another question, only you can answer.

But what about the value of the financing?

By value, we define that the financing is ‘cheap’. In the context of this rights issue, we want to see if CLINT is getting value for money, or if it’s overpaying for what it’s getting.

CLINT argues that this acquisition would raise the net leasable area by 3.8x. But whether or not this 3.8x increase in leasable area will flow through to income for the REIT, remains to be seen.

For example, one big highlight is the development of a data centre at the ITPH compound.

Whilst this sounds nice and sexy, we do know that capitalisation rates for data centres have been declining due to increasing investor interest.

:max_bytes(150000):strip_icc()/Capitalizationrate-122a804a049444c788fceb400986e3df.jpg)

Mapletree Industrial Trust, which acquired 14 data centres in the US in August 2020, shared in their 2021 Annual General Meeting the following.

CLINT then points out that

Approximately S$91.2 million (will be) applied towards the extension of ongoing funding to the developers of the properties known as aVance A1, HITEC City, Hyderabad (“aVance A1”)3 and Gardencity, Hebbal, Bangalore (“Gardencity”)4 to part fund the development and construction of aVance A1 and Gardencity,

in return for annual coupon rates of at least 11.0%.

In other words, it’s taking on the risk of funding the project, in exchange for a coupon payment of 11%.

And after the completion in the second half of 2024, it can then lease the properties out.

It’s win win. As a unit holder, you get to enjoy coupon payments even when the project is not even built.

It sounds like great value.

The quality of the business?

Here we want to look more into the quality of the assets that underlie CLINT.

Don’t get me wrong.

I’m a big fan of CLINT and think that the management team comprising CEO Sanjeev Dasgupta, does know what they are doing.

They are riding on the Indian growth wave. And the quality of their properties are extremely good.

But when I compared them to others like Mapletree Industrial Trust and FLCT, we did see that their metrics in terms of returns on capital employed weren’t as good.

Of course, the measure of a REIT primarily is DPU, rather than return on capital employed.

And if we look at their yield compared to others in the market, they are better.

How does this compare with others?

For this article, we went back to look at some of the best performing REITs over the years to see what they did in terms of rights issues, to see if you should continue to hold CLINT, subscribe, or drop them.

We looked at Mapletree Industrial Trust, and what it cleverly did with a private placement, and a rights issue to fund its acquisition of data centres in 2021.

Balancing yield growth with share price growth

When REITs need money to grow, there are often two options.

How they choose to do that is indicative of how much they take the interests of the retail investor in mind.

Sure, with IREIT and their continual preferential offerings to retail investors, it gave more units at a discount, but retail investors may not have realised the continual drop in the share price.

With CLINT, I think they do consider both retail and institutional interests.

That’s why they have continued to use both private placements and preferential offerings to grow.

I’d say this is a good buy, though you have to be prepared to wait for at least 3 years, post 2024, post the development of Gardencity and aVance, for there to be a growth in their share price.

Great article – very well detailed and researched!

Was wondering what site did you use to compare the various reits?

Hello! Just wanted to share that I used Stockopedia, which has a two-week trial. Hope this helps!