A month ago, I made the painful decision to exit Avarga. And if you’ve held on to Avarga over the past years, here’s why you might reconsider your position.

The initial thesis

I confess.

I went into Avarga because I was attracted by how Tong Kooi Ong, and later Ian Tong, his son, wrote their annual letters.

It read just like Warren Buffett. And being a Warren Buffett fanboy, I just couldn’t resist.

But the wider thesis were 3 factors. When we took the position in July 2021, it was

- Their dividend policy was throwing off incredible amounts of cash at a yield of

- Their earnings had grown phenomenally over the years

- The management seemed to be great at acquiring businesses at a fair value, like the Myanmar power plant, and the Taiga business

This was a heavy conviction bet.

I usually start positions with a $2-3k bet, but this was a $11,000 bet.

It showed how confident I was in Avarga.

In my mind, I thought that even if the thesis didn’t play out, I would at least have the chance to get dividends.

Much has changed

First they axed their dividend policy on 26 February 2022.

But of greater concern to me was the fact that they had no control over the capital from Taiga.

This meant that the only capital they can deploy is the capital that is generated from the power plant and the paper business.

This is a really, really important point to note.

Whilst they can boast of a top line of $2.4 billion in revenue, much of that is from Taiga, and not Avarga.

And the growth that Taiga has will end up being reflected in Taiga’s share price, rather than directly accruing to Avarga.

So what’s more vital is to look beneath the numbers and to split the revenues segmentally, to see how much capital Avarga has to deploy.

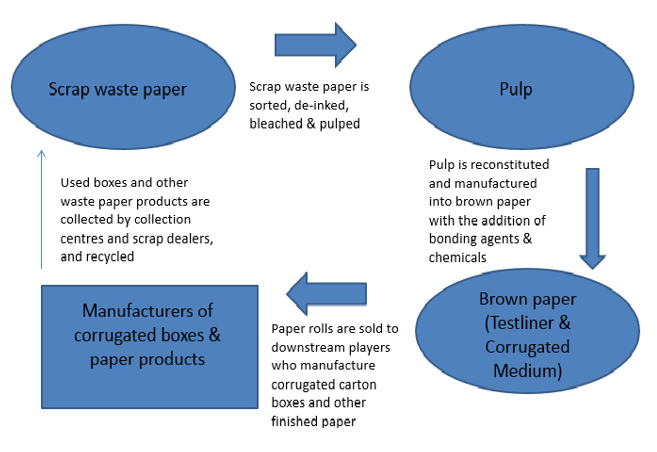

Can they turn the paper business around?

If you look at 2018 to 2022, it doesn’t make for easy reading. They have consistently had lower and lower pre-tax profits.

Ian wrote in the 2022 Annual Report:

Going forward, the operating environment remains challenging.

He attributes the loss to the Chinese companies who’ve set up business in Malaysia as a result of China’s ban on the imports of waste materials.

With the scale and volume of their businesses, they can easily out-compete Avarga, which sells cardboard.

There’s no guarantee Avarga will win.

Management has re-evaluated the business model and will embark on a plan to restructure the operations, including a revamp of our product range.

However, there is no guarantee of success and we must be prepared to make difficult decisions.

Are the Tongs turnaround artists?

They appear to be better at investments than turning ailing companies around.

Whilst much credit must be given to them for turning the paper business around, improving its operational efficiencies, and controlling costs, moving it to a place where it’s now in the black, the influx of competition may just be a little too much for them.

Michael Watkins points out in his book ‘The First 90 Days’ that most executives do one function well, but rarely do well across the whole range of functions in his STARS model.

I’m sure the Tongs will know when to quit.

This is not Berkshire

Whilst I admire Tong for emulating Berkshire as an investment vehicle, this is not Berkshire.

Early on in Berkshire’s journey, Buffett bought National Indemnity (NICO), a small insurance company. This allowed him to have float (the premiums that customers pay to be covered), which he reinvested in better returning businesses.

Moreover, our growth would not have been impeded for nearly two decades by the unproductive funds imprisoned in the textile operation.

Whilst Buffett uses the above explanation to explain why he made a ‘colossal mistake’ in using Berkshire to buy NICO, I found this a great analogy for what Avarga is doing now.

Some of the funds they have used to take over businesses are now imprisoned in heavy, capital intensive industries like lumber trading and paper manufacturing, which leaves them little room for making the value investments that Tong is known for.

It also means that moving forward, there may be less and less of those investments which pay off and bring cash to the Avarga business.

And that’s why we quit

Call us impatient, but when you see warnings like that below, it does make you think that there are better opportunities elsewhere.

Sure, we realised a $3000 loss, and a 36% loss in value, but I think it was better that we eventually did get out.

There are many better opportunities that abound in the market.

You might just want to reconsider your position.

I’m sure that they will eventually turn things around.

I think that

- It begins with a close hard look at the paper business, and potentially selling it off to one of the bigger Chinese companies that have set up market

- Reinvesting the money in a business that is not as capital intensive,

- Making greater room to manoeuvre in the market and pick up value businesses in the market

I made a colossal mistake here in thinking that Taiga’s money was Avarga’s money to invest.

Don’t make the same.